A common example of contra account is the Accumulated Depreciation account, which is used to offset the value of fixed assets in the balance sheet. As the fixed assets are depreciated over time, the accumulated depreciation account increases and the fixed assets account decreases, but the net effect is zero. Using the rules above we can now balance off all of Edgar Edwards’ nominal ledger accounts starting with the bank account. • Both sales and purchase ledgers are considered as an internal database, usually maintained by the accounting department.

This is the amount XYZ Coffee Shop should see when they look at the accounts payable balance in their general ledger. The purchase ledger will also include transactions related to any discounts received from suppliers, including the amount and date of the discount, as well as any discounts lost. The purchase ledger is an important tool for managing and tracking a company’s debts and for ensuring payments are made accurately and on time. By reviewing the purchase ledger, a company can see how much it owes and to whom, allowing it to effectively manage its cash flow and maintain good relationships with its suppliers.

What is the Purchase Ledger Control Account?

Once the amount and the invoice total is correct you will be able to

select Save or Save & Exit. It’s easy to track your expenses from anywhere with online invoicing software like Debitoor.

Designed for freelancers and small business owners, Debitoor invoicing software makes it quick and easy to issue professional invoices and manage your business finances. As per the golden rules of accounting (for personal accounts), liabilities are credited. In other words, the giver of the benefit is a liability to the one who receives it. Accounting software such as QuickBooks, FreshBooks, and Xero are useful for balancing books since such programs automatically mark any areas in which a corresponding credit or debit is missing.

purchase ledger

Sales ledger that falls under the system of accounts, always records all credit sales transactions of a particular organization. Main purpose of maintaining a ledger is to record and monitor debtors of the business. The sales ledger control account is a total for the trade receivables.

15 Superior Bookkeeping Software for 2023 – CitizenSide

15 Superior Bookkeeping Software for 2023.

Posted: Mon, 21 Aug 2023 06:14:38 GMT [source]

The total amount owed to suppliers at any given time, as shown by the purchase ledger, should equal the balance on the accounts payable account shown in the general ledger. The individuals and other organizations that have direct transactions with the business are called personal accounts. PLCA indicates total trade payables at a given point in time, and since trade payables are personal accounts, PLCA also operates according to the golden rule for personal accounts. Purchase Ledger Control Account (PLCA) is a summarized ledger of all the trade creditors of the entity.

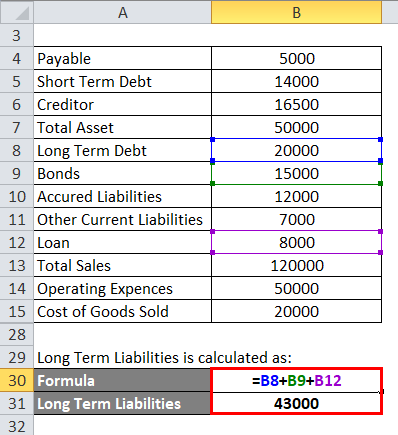

Purchase Ledger Control Account (PLCA)

• The final amount of the sales ledger is transferred to the sales ledger control account via general ledger. Meanwhile, the final amount of the purchase ledger is transferred to the purchase ledger control account via general ledger. Purchase ledger is a book of accounts that records all credit purchase transactions of an organization. Main aim of maintaining a purchase ledger is to keep detailed purchase records and monitor creditors. It contains individual accounts of different creditors and other central information such as receipt numbers, VAT, purchase order numbers, payment period and payment terms. The purchase ledger control account is a debit account, which means that it increases when there is a purchase made, and decreases when a payment is made to a supplier.

- C) Prepare a Statement altering the total of the sales ledger balance to agree with the new sales ledger control account balance.

- The individuals and other organizations that have direct transactions with the business are called personal accounts.

- We need to work out the balance on each of these accounts in order to compile the trial balance.

- To begin, enter all debit accounts on the left side of the balance sheet and all credit accounts on the right.

- It is to be remembered that if the Debit balance is transferred from the sales ledger to the purchase ledger or the credit balance is transferred from the purchase ledger to the sales ledger.

This Control Account typically looks like a “T-account” or a replica of an Individual Trade Payable (Creditor) account. But instead of containing transactions of invoices, returns, and payments related to one creditor, it contains summarized transactions of invoices, returns, and payments related to all the creditors in the business. B) Prepare an amended sales ledger control account, extracting the relevant information from the list of errors given above. Control accounts give a summary of all the individual accounts that are in the sales and purchases ledger. It provides a nice total which can be used in the statement of financial position. In addition it is a double check to ensure we have not made an error or any fraud has taken place.

Course content

The account will contain the total amount owing to suppliers, and it is usually reconciled with the supplier’s statement to ensure the accuracy of the purchase ledger. When you have finished, check that credits equal debits in order to ensure the books are balanced. Another way to ensure that the books are balanced is to create a trial balance.

Thus, Purchase Ledger Control Account is credited if its balance increases & debited if its balance decreases. The balance of the PLCA should equal the sum of the balances of the individual supplier accounts. Purchase Ledger Control Account is also referred to as a “Trade Creditors Control Account”. It indicates the total amount a business entity owes to its suppliers at a particular point in time. Therefore, it is a “short-term liability” for the business entity and forms part of the balance sheet. To begin, enter all debit accounts on the left side of the balance sheet and all credit accounts on the right.

This may happen when a debit entry is entered on the credit side or when a company is acquired but that transaction is not recorded. Similarly, a credit ticket may be entered into the general ledger when a deposit is made, but it needs an offsetting debit ticket, either at the same time or soon after, to balance the books. In Debitoor accounting & invoicing software, the double-entry bookkeeping method is built-in, meaning that when you enter an expense, you can also enter payments on the expense for specific suppliers. The payments show up automatically on internal financial statements that can be generated with a click. They must also ensure that the amount listed in the control account is the total of each of the amounts owed by a business to each supplier.

At the end of a specific period, these ledgers are summarized and the total amounts are recorded in respective control accounts. As sales and purchase ledgers are two of the sub-ledgers used in the practice of accounting, it is useful to know the difference between sales ledger and purchase ledger. Sales ledger and purchase ledger can be identified as two sets of sub-ledgers used to record detailed sales and purchases data. The purchase ledger control account is a control account used in double-entry bookkeeping and accounting systems to summarize and reconcile the activity in the purchase ledger. The purchase ledger is a subsidiary account that records all the transactions related to the purchase of goods and services from suppliers. • Information comprised in sales ledger and purchase ledger helps to reconcile the creditors and debtors status with the balance of respective control accounts.

The following errors have been discovered since the sales ledger control account was prepared. A) Extract the relevant information from above and prepare the sales ledger control account for the month ended 31 May 2003. When a business purchases goods on credit, an entry is made to the accounts payable account, which is a liability account. When the business pays off the credit, an entry is made to the cash account and a corresponding How to balance purchase ledger entry is made to the accounts payable account, which is a contra account to the accounts payable account and the net effect is zero. A contra account is an account that is used in double-entry bookkeeping to offset the balance of another account. Contra accounts have opposite normal balances than the account they offset, for example if the account it offsets is a debit account, the contra account will have a credit balance.

At any given time, the total of the outstanding amounts in the purchase ledger should match the accounts payable balance in XYZ Coffee Shop’s general ledger. Purchase ledger control account is a part of a balance sheet and a short-term liability. Also known as the “Trade creditors control A/C”, it shows the total trade creditors of a company at a given time. In other words, it shows how much in total a business owes to its suppliers at a particular point of time, i.e. the total of Accounts Payable. A control account exists for both creditors and debtors and is used to ensure that there are no errors in the ledgers (that any sub-ledgers match up with the general ledger). Since it indicates the total trade payables, it shows a credit balance and the modern rule of accounting cannot be broken under any circumstances.

The purchase ledger shows which purchases have been paid for and which purchases remain outstanding. A typical transaction entered into the purchase ledger will record an account payable, followed at a later date by a payment transaction that eliminates the account payable. Thus, there is likely to be an outstanding account payable balance in the ledger at any time.